Towards a degrowth policy sequence

Articulating policy priorities for transforming growth-dependent macro-financial regimes

Written by Emmanuel Bamdeis

Cover illustration: Eleanor Shakespeare

If GDP growth leads to the destruction of humanity’s life support systems, but the absence of growth produces widespread deprivation due to current economic structures, the solution must be to transform these economic structures, which uphold and cement capitalist macro-financial regimes. To this end, degrowth proponents have formulated many ideas and lists of recommendations, but so far limited progress has been made in defining clear policy priorities and articulating them in a structured and dynamic manner that appears feasible from a material and technical as well as technocratic and democratic perspective.

Yet, history provides instructive examples about why structural change is better understood as the result of a sequenced path of policy action rather than as the spontaneous result of a policy “Big Bang”. A good example is the painful transformation of former centrally planned economies into market economies through the “Big Bang” approach of the IMF, which recommended the simultaneous liberalization of all markets, an approach that proved disastrous. In comparison, the gradual and sequenced approach pursued in China, which still retains control over the convertibility of its currency and domestic financial markets, following Keynes’ advice “to let finance be primarily national”, was more successful at achieving its declared objectives, despite all its democratic and other shortcomings.

Back to degrowth: is the time ripe to formulate a policy sequence for its implementation? What would be the main principles and elements of such a sequence? And what would the degrowth movement gain from attempting to translate and simplify its rich vision into the format of a generic policy sequence for the Global North? Those are some of the questions discussed here.

Moving beyond static policy lists and empirical modelling

The difficulty to make degrowth research directly relevant for policy is partly due to the absence of a well-established unifying theoretical framework able to integrate degrowth proposals into a coherent, realistic and inspiring narrative, which any transformative policy vision requires. Many contributions falling under the post-growth and degrowth umbrella focus on single topical issues (e.g., energy, food, fast-fashion, etc.) and thus lack the bigger picture coherence that is needed to communicate degrowth to a wider and more skeptical audience.

Integrative empirical frameworks, such as multi-sector integrated assessment models (IAMs), are helpful to investigate the material and technical feasibility of degrowth scenarios. Yet, such frameworks generally remain based on flawed neoclassical assumptions, which focus on consumer preferences and price adjustments as the main means of transformative change. They are thus ill-suited for fostering reflection on policy and institutional transformations, which is required to make the case for the democratic and technocratic feasibility of degrowth. For this, a more qualitative yet integrative theoretical framework is required.

Towards synthesis and dynamic policy sequences

Recent synthesis work by post-growth and degrowth academics alongside initiatives emerging in the international policy arena significantly contribute to highlighting key policy areas and options and structuring ideas into useful policy catalogues. Yet, they still fall short of raising the thorny questions of policy selection, ordering and timing that underpin the elaboration of policy sequences. Indeed, many policies favoured by degrowth proponents (e.g., green job guarantee, working time reduction, wealth and income caps, etc.) have long been championed by other movements, mostly in the camp of the techno-candid growthist or Keynesian left.

What distinguishes degrowth, however, is the combination of progressive policies fostering democracy, equality and economic security together with policies reducing energy and material throughput, thus reducing economic activity, private consumption and growth. In other words: living well within limits! Because degrowth is macro-financially destabilizing under capitalism and its proponents have not yet made sufficient attempts to think through its conditions of feasibility and anticipate its consequences, implementing degrowth still appears as a daunting challenge, even from a narrowly technocratic point of view.

Regardless of whether one argues that states, revolutionary labour unions or broader coalitions of democratic forces must be in the driver’s seat to ensure institutional coordination during the degrowth transition, one weakness of degrowth proposals is the lack of blueprints for reflecting on the most appropriate sequence of action. A “Big Bang” approach is doomed to fail and cause chaos with the potential to reinforce reactionary political forces. So, which institutions must change? And where to start? The latter question appears of paramount importance, especially if the answer to the former question is “everything”.

Institutional transformations for degrowth: an approach through the lens of green macro-financial regimes (MFRs)

In a recent working paper titled “Towards a green post-growth macro-financial regime? Implications for the Global South of imperfect technology and sufficiency policies in the Global North”,¹ Elena Hofferberth and I tackle the challenge of formulating a degrowth policy sequence. Formulating such a sequence requires identifying and ordering key policy steps for establishing a post-growth macro-financial regime (MFR), defined as “the combinations of monetary, fiscal, and financial institutions that shape the creation and allocation of credit/money”. The four key steps of our proposal for a degrowth policy sequence are represented in a stylized manner in Figure 1 and described in more detail below and in the paper, while the main institutional and policy features of the post-growth MFR are summarized in Table 1, which offers a comparison along six dimensions with other MFRs discussed in the literature.

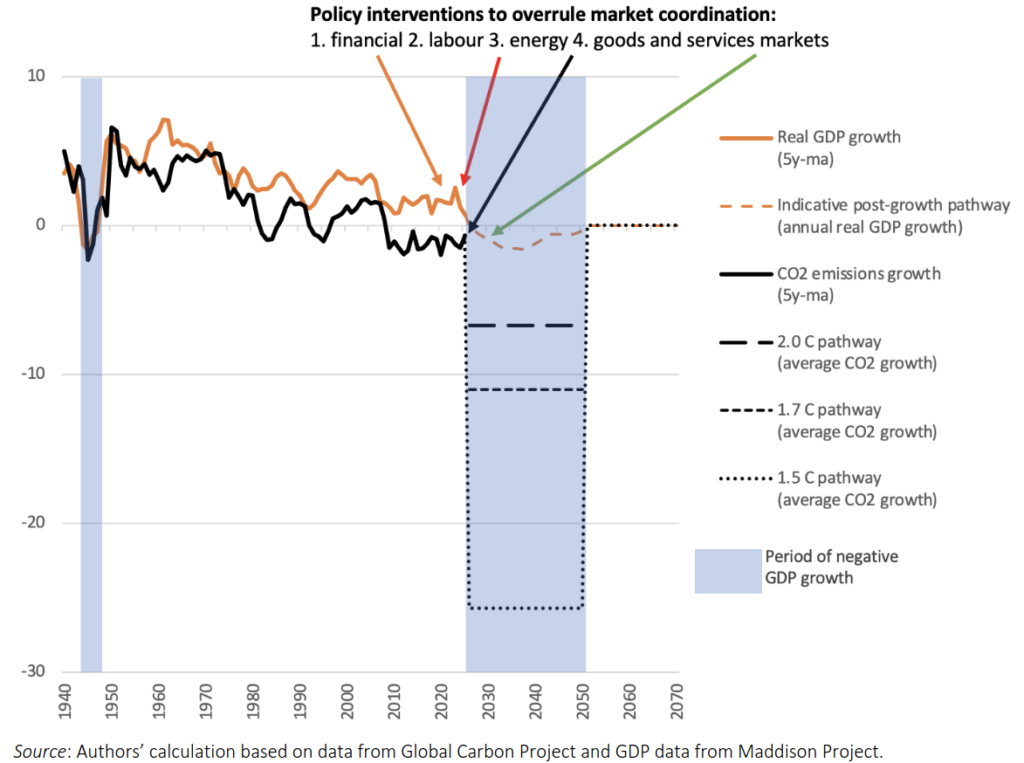

Figure 1: Stylized four-step degrowth policy sequence: overcoming structural constraints weighing on growth-dependent MFRs in the Global North to establish a post-growth MFR able to deliver on Paris-compatible green and just transformations

Growth rates of GDP and carbon emissions from fossil fuel, Annex B countries ² (Percentage)

Table 1: Main features of “green” macro-financial regime

The MFR theoretical framework was developed by critical macro-finance academics. It offers the advantage of building on historical insights, an understanding of how macro-relevant sectoral balance sheets are interrelated, and institutional and policy analysis to reflect on structural transformations required for the “green transition”, which we claim must take the form of a degrowth transition towards post-growth societies.

Whereas much critical macro-finance literature keeps assuming “green” growth may work or does not engage with the consequences of negative economic growth, we take climate science seriously. We postulate that technical “solutions” for climate mitigation are very imperfect and, alone, insufficient for achieving Paris climate goals and respecting other planetary boundaries. Consequently, we foresee that demand-adverse (i.e., consumption- and GDP-adverse) sufficiency policies discussed in the last IPCC reports will be key during the green and just degrowth transition that is required to stabilize climate and protect ecosystems.

The lead question of our paper is thus “what MFR can best discipline private capital and support sufficiency policies reducing private production and consumption in the Global North to complement the insufficient emissions mitigation that can reasonably be expected from higher investment in (imperfect) “green” technologies?” To answer this question, we do not only attempt to draw policy inspiration from

- developmental states, which managed to discipline private capital and rapidly reshape investment, but also from

- states acting in periods of emergency (e.g., wars, pandemic) to reduce private consumption (and related inequalities),

which both represent simultaneous macroeconomic imperatives for implementing degrowth.

Structural constraints to structural transformations

The paper identifies several structural constraints that obstruct and will shape the degrowth transition toward a post-growth macro-financial regime, starting from the current capitalist context:

- Imperfect markets: Markets consistently fail to provide public goods, including the level of green investment required for timely climate mitigation.

- Imperfect technologies: Existing climate mitigation technologies, such as negative emissions technologies, are insufficient to meet Paris targets at the necessary scale and speed. As a result, technological solutions must be complemented by demand-adverse sufficiency policies starting in the Global North.

- Growth dependencies: Capitalist economies depend on growth for macro-financial, social, political, and ideological stability, making it impossible (without significant institutional changes) to implement policies that intentionally reduce aggregate demand.

- State limitations: States structurally tend to prioritize growth and the interests of capital, which constrains their ability to implement transformative policies.

The hurdle of political and economic democratization

Structural political economy hurdles are massive and widely acknowledged, including in recent synthesis works mentioned above, which all stress the centrality of democratizing political and economic governance for enabling transformative change. Indeed, resistance to change is generally highest at the top. This means capitalist firms and states will never on their own rapidly implement sufficiently ambitious structural transformations. A central degrowth challenge thus lies in building and strengthening institutions and actors capable of supporting such transformations.

While most people intuitively understand the notion of democratization and how it could be implemented in the political field, the case for economic democracy and how to proceed for transforming growth-dependent MFRs may be less obvious. Importantly, communicating and educating about economic democratization of macro-financial institutions, as we attempt to do in our paper, could highlight its technocratic feasibility and hence its desirability and democratic feasibility.

In a nutshell: a degrowth policy sequence for transforming growth-dependent MFRs

The core principle for establishing a post-growth MFR is to create institutions, especially macro-financial institutions and policy arrangements, whose stability and viability does not depend on continued growth. Based on an analysis of growth imperatives currently weighing on private investors, the government and labour, the paper stresses that growth-dependent MFRs cannot sufficiently discipline private capital and support the demand-adverse sufficiency policies required in the Global North, because their stability and viability depend on continued growth. Hence such MFRs cannot deliver Paris-compatible climate stabilization.

Not all social actors are equal in the face of macro-financial destabilization, however. The balance sheets of worker households are most vulnerable to a decline in economic growth and, concretely, their livelihoods are most vulnerable to a decline in private consumption. In addition to social harm, their vulnerability entails the risk of upending macro-financial, social and political stability on the road to net zero. Consequently, policy proposals for green MFRs aiming to maintain macro-financial stability must encompass institutions on which the livelihoods of workers directly depend, which goes beyond the narrow monetary realm.

In the current context of almost ubiquitous markets, this means focusing not only on institutions shaping taxation, fiscal and monetary policy, and financial markets, but also on those framing labour, energy, goods and services markets and their necessary reform to support public provisioning, price controls and rationing schemes, which are key for implementing sufficiency policies at the scale required for a green and just transition.

Because ensuring and financing the economic security of people is a pre-requisite for a stable green “transition”, this goal must play a central role in determining the sequence of action for establishing a post-growth MFR. The generic policy sequence proposed in our paper sketches the following ordering of four major policy interventions to weaken market coordination and disable related growth imperatives (which are discussed in more detail in the paper):

- Financial markets

- Labour markets (and markets for the most essential goods and services, such as housing or food)

- Energy markets

- Other markets for (intermediate and final) goods and services

The sequential logic of these economic policy transformations can be summarized as follows:

- Policy interventions to implement non-market coordination in financial markets should start first. If money is power, as formulated by Adam Smith, then money creation epitomizes the political power to decide over investment, the allocation of human and material resources, and the future of social production. And any political project aiming to transform social production, such as degrowth, should think hard about how to transform the macro-financial institutions governing the creation and allocation of money under the prevailing capitalist social order. In contemporary capitalism, money creation is overwhelmingly left to private financial institutions blindly chasing short-term profit opportunities. To support less profitable or unprofitable investment, such as a rapid build-up of green energy supply or stranding fossil fuel assets and retrofit related infrastructure, public institutions must stop delegating the power of money creation to for-profit private finance. Instead, they must expand their own fiscal spending and redistributive power for ecological and social purposes, while simultaneously developing credit guidance and restraining capital mobility.

- Because a timely phase out of fossil fuels in Global North countries will reduce economic growth and thus destabilize market coordination, squeezing out poorer households, interventions to overrule market coordination in labour markets (and markets for the most essential goods and services, such as housing or food) must imperatively precede interventions in energy markets. Put simply, a timely phase out of fossil fuels cannot be implemented without broad social support which can be fostered through the participation of people in the design of “Just Transition plans” and measures that safeguard people’s livelihoods. They could include the prior creation of a green job guarantee and/or the possibility for securing productive autonomy, for instance through control over means of production or through facilitated access to land. The establishment of Universal Basic Services, i.e., guaranteed access to essential goods and services at low or no cost represents another means to protect people against economic shortfall in case of labour market disruptions. Importantly, a number of interventions in markets for the most essential goods and services, such as rent and food price controls, could contribute to alleviating fears of market exclusion and to building broad support for a timely phase out of fossil fuels.

- Only after the economic security and livelihoods of worker households is guaranteed public institutions can intervene in energy markets to phase out fossil fuels and reduce aggregate energy use. This can be achieved through dedicated energy rationing schemes, without creating economic distress and social and macro-financial instability.

- Finally, as historical examples illustrate, managing declining consumption also requires intervening in other (intermediate and less essential final) goods and services markets through price controls and rationing schemes.

The paper then presents the main institutional and policy features of a post-growth MFR in more detail, including possibly supportive international coordination, before also discussing implications for the Global South, which cannot be summarized here. For more, read the paper!

¹ The research is a part of Elena Hofferberth’s project “CliMacro: Alternative Macro-Financial Frameworks for Climate-Just and Post-Growth Futures”, which has been supported by Swiss Network for International Studies (SNIS) and the REAL project.

² Annex B countries regroup 37 (“developed” and former transition economies) countries who first committed to achieve emissions mitigation targets under the Kyoto Protocol.

Emmanuel Bamdeis, PhD, is an economist affiliated with Research & Degrowth International (R&Di).

The opinions expressed in the text do not necessarily reflect those of R&Di, but are those of the author.